Summary

- Sales in the King’s Road were down -7% in August 2023 compared to August 2022, ahead of Knightsbridge but behind Marylebone and Sloane Street. On a Year-to-Date (YTD) basis, sales are down -3%, which is weaker than its comparators.

- The key drivers of this decline in sales 2023 were a -4% decline in customers and a -3% drop in Average Revenue Per Customer (ARPC).

- Of the four of the largest retail sectors (which together account for over 90% of sales), three saw declines in sales compared to August 2022. Fashion, the largest sector, saw a -19% decline, Food & Drink was down -14% and Health & Beauty was down – 8%, while there was positive +8% growth in Grocery.

- Of these sectors, only Health & Beauty shows sales growth on a YTD basis (+3%)

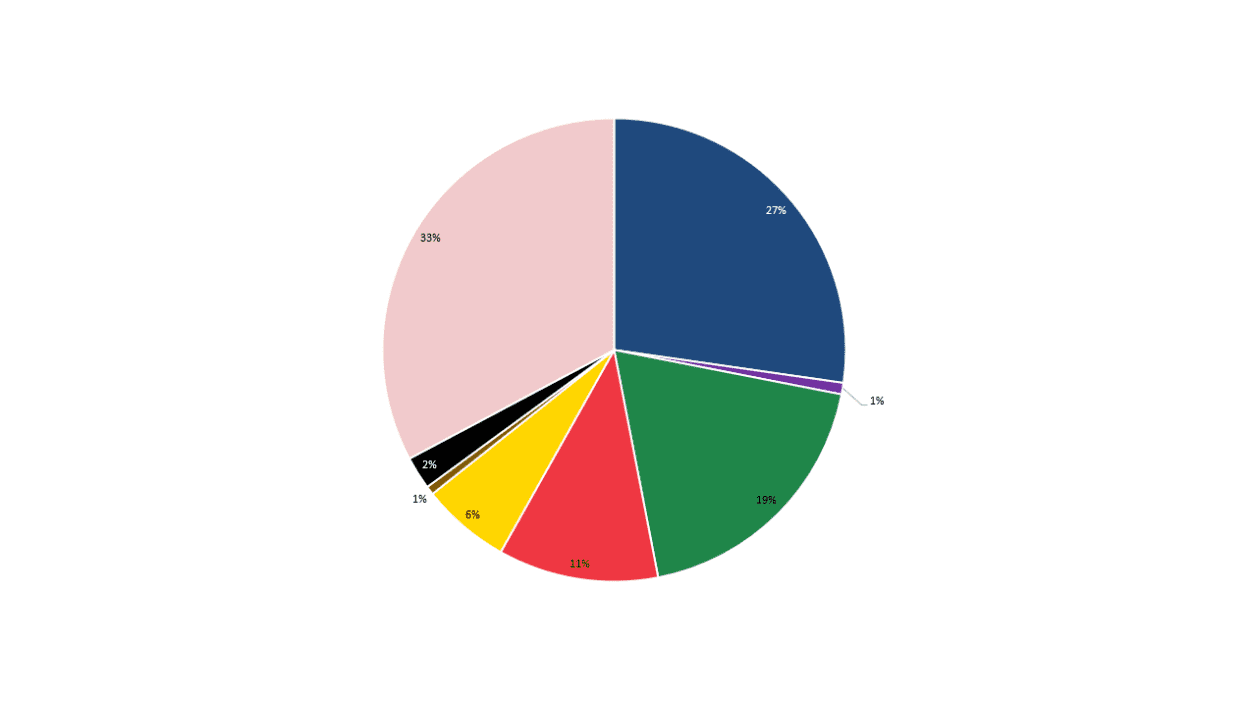

- The share of sales from Chelsea & Kensington in August 2023 was 28% compared to 25% in August 2022. This remains consistent with the trend in 2023 of a small increase in the share of sales to locals.

- This was offset by a decline in the share of sales to customers from Rest of GB. In August 2023 this was 36%, down from 39% August 2022 (which was the peak month in 2022).

See the full report here.